In the previous article, we talked about remittances in India, the largest receiver of remittances worldwide.

Now let’s look at one of the largest markets for outbound remittances, the Middle East & North Africa (MENA) region.

According to a recent World Bank report, total remittance outflows from MENA countries amounted to USD 109 billion in 2017. Mostly originating from the GCC countries, over a third of these remittances went to India. The World Bank also estimated the average cost of remittances from the MENA region at over 7%, making this a sizeable business for the incumbents. These figures do not include the informal channels (such as Hawala). Those can be hard to track, but are estimated to be as big as the formal channels.

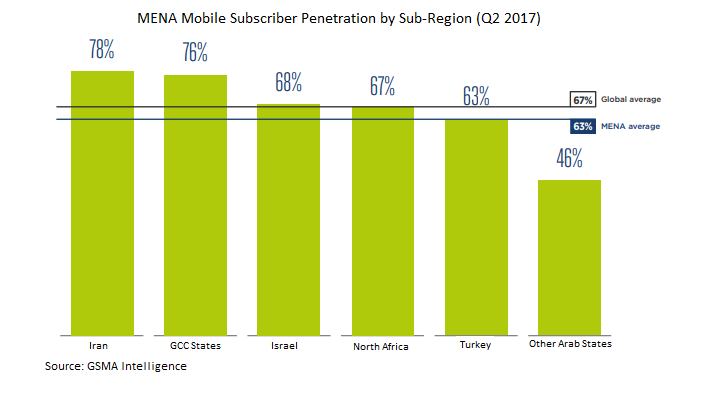

The huge potential for tech disruption in this market, given the fees and growing mobile penetration, is not lost on innovators.

We will look at efforts being made to digitize this industry in the region from two fronts – the incumbents (banks and MTO’s) and the newcomers (tech start-ups).

The Incumbents

- Banks

Banks prefer to keep the fees and customers within their own sphere of services. Most of the large regional banks allow their customers to send money internationally from their own online bank accounts. However, customers end up paying more for this convenience. As reported by World Bank (June 2018), banks charge an average of 10.4% on global remittances, compared to an average cost of 6.99% across channels.

These costs have been steadily declining, and banks are now keen on making these services cheaper and faster in order to retain their customers. Mashreq Bank, a leading UAE-based bank, launched their Quick Remit service in 2017, offering instant online money transfers for their customers to banks in Pakistan and India. A similar service called Direct Remit was launched in 2014 by Emirates NBD, another major UAE-based bank. Direct Remit offers intra-day money transfers to Emirates NBD customers in major corridors such as India, Pakistan and Philippines.

A number of regional financial institutions, including UAE’s RAK Bank and Oman’s BankDhofar, have partnered with Ripple’s enterprise blockchain network RippleNet. This would enable them to process speedy transfers to over 100 institutions worldwide that are also on Ripple’s network, such as India’s Axis Bank.

- Money Transfer Operators (MTO’s)

MTO’s are still the preferred formal channel for millions of blue-collar workers across the Middle East. These expatriate workers are largely un-banked, and process regular (usually monthly) small-ticket cash remittances through agency outlets. MTO’s are also keen to service the white-collar expatriates, which process less regular but larger size online transfers. They are investing increasingly in online platforms to offer convenient solutions across various corridors.

UAE Exchange, one of the largest MTO’s, has been investing heavily in online and offline money transfer platforms over the years. Similar to banks, UAE Exchange also joined the Ripple network to process real-time money transfers. It acquired Remit2India, an online money transfer business servicing Indian expatriates, in 2017. Xpress Money, a subsidiary of UAE Exchange, launched an app called Xopo (now Xopoto) in 2016, allowing customers to send money to their contacts on social media platforms such as Facebook and WhatsApp. Xpress Money also partners with banks such as UAE-based RAK Bank to give regional banks access to global locations. Bank customers get to transfer money from their online bank accounts or credit cards, allowing recipients to pickup cash from Xpress Money’s agent locations worldwide or receive funds online.

Other MTO giants have also started looking at digitization more seriously. In March 2018, Mynt, a FinTech firm, announced a partnership with MTO giant MoneyGram to allow families of Filipino expatriates to receive money directly on their mobile wallets. In August 2018, Western Union reported a 22% increase in consumer revenue on its online transfer business.

The Newcomers

Well-funded international start-ups have been eyeing the lucrative Middle East corridors. Some interesting local start-ups have also emerged and are gaining traction. We will discuss a few of the prominent international and regional names in this space.

TransferWise, the UK-based remittance unicorn which have raised USD 400 million and are valued at USD 1.6 billion as of November 2017, set up their Middle East office last year. As per their website, they have begun remittance services in the region, starting with UAE, Morocco, Turkey and Egypt.

WorldRemit, another UK-based remittance service provider, also allows GCC-based customers to send money to recipients worldwide. The 8-year old start-up has raised USD 220 million and was valued at USD 670 million at its last fund-raising round in December 2017. With its deep pockets, the company has expanded its reach, allowing customers to send money from over 50 countries to recipients in 148 countries (as per reports in December 2017). For recipients in India, for example, senders can wire money to bank accounts, or fund airtime top-ups directly to mobile phones.

Now Money is a UAE-based fintech start-up focused on providing basic mobile payment and remittance services to the large unbanked low-income migrant populations in GCC countries. The 3-year old company has raised USD 2.3 million, as reported by Crunchbase. It claims to have partnerships with multiple MTO’s to present cheaper remittance options to its customers (it earns a share of the remittance fees from the MTO’s).

Denarii Cash is a UAE-based blockchain start-up, which aims to offer a multi-currency (including cryptocurrencies) payment and money transfer services to its customers. Instead of the MTO or banking routes, the start-up plans to employ Stellar’s (a remittance-focused Ripple rival) blockchain to enable transfers. It will also engage with a network of individuals and businesses to act as physical cash deposit and withdrawal points (similar to on and off-ramping agents used by MTO’s) to facilitate customers without bank accounts. As per their white-paper, the start-up is planning to raise funds via a token sale in September 2018.

What to Expect in the Future?

Projects like Denarii Cash are ambitious in scope, but certainly interesting. We can expect more blockchain start-ups to launch in this region in the near future.

Stellar’s blockchain and its associated cryptocurrency (Lumens) obtained a Shariah compliance certificate from Bahrain’s Shariah Review Board in July 2018. This should enable Stellar to partner with start-ups as well as established Islamic financial institutions, looking to build Shariah-friendly payment and remittance applications on top of Stellar’s blockchain.

What does it mean to be Shariah compliant for a blockchain provider or a cryptocurrency? Is it just a marketing gimmick or a real opportunity that would set them apart from their conventional counterparts? Let’s explore that in the next article.